Helpful Links

- Iowa Fuel Tax Forms

- GovConnectIowa – Register for Licenses or Permits

- GovConnectIowa Help

- Change or Cancel a Fuel Tax License

- EasyPay Iowa – Electronic Payment Options

- Fuel Tax Licensee Listing

- Fuel Tax Monthly Reports

- Retailers Fuel Gallons Annual Reports

- Interest Rates

- CNG Iowa Requirements (pdf)

- Schedule Upload Template (excel)

- Iowa Schedule Codes (pdf)

- Fuel Product Codes (pdf)

- Motor Fuel Tax Information by State

Subscribe to Iowa fuel tax news

Iowa Fuel Tax Rate Changes Effective July 1, 2024

The Iowa fuel tax rate for undyed biodiesel classified as B-11 to B-19, undyed biodiesel classified as B-20 or Higher, and ethanol blended fuel classified as E-15 or Higher and Alcohol will change July 1, 2024. All other Iowa fuel tax rates will remain the same. All rates and effective dates are available under the Iowa Fuel Tax section of the Iowa Fuel Tax Rates and Descriptions page.

Fuel Tax Inventory Return for 2024

Per Iowa Code 452A.85, an Iowa Fuel Tax Inventory Return will be required for persons having title to fuels in storage and held for sale on July 1, 2024, where there is an increase in the tax rate in excess of one-half cent per gallon. Fuels classified as B-11 to B-19 and fuels classified as E-15 or Higher will have fuel tax rate increases of more than one-half cent per gallon and will be required to be reported on the 2024 Iowa Fuel Tax Inventory Return due July 31, 2024.

The 2024 Iowa Fuel Tax Inventory Return shall be submitted electronically by persons having a motor fuel retailer account or a motor fuel eligible purchaser account. The return shall be submitted on paper for persons without an account.

For retailers and eligible purchasers, the returns shall be filed electronically via GovConnectIowa by clicking on the link “File 2024 Motor Fuel Inventory Return” shown on the respective account. If you have both a retailer account and an eligible purchaser account, only one return needs to be filed, file it on the retailer account.

If you do not have a retailer account or eligible purchaser account and need to submit an inventory return, please complete and submit the paper form 2024 Motor Fuel Tax Inventory Return, 80-020, located on tax.iowa.gov.

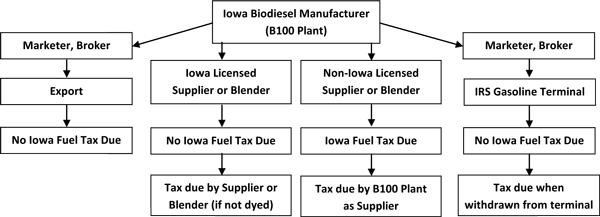

Please note a return is not necessary for undistributed fuels in registered IRS gasoline terminals or undistributed fuels in storage facilities destined for registered IRS gasoline terminals as the appropriate fuel tax rate will attach to those fuels once they reach the point in the distribution process where the tax attaches, which is known as “withdrawn from terminal”.

Income Tax Credits and Sales/Use Tax Refunds for Use, Sale, and Production of Fuel

Income tax credits have been instituted in recent years that relate to the use, sale, and production of fuel; however, these credits do not impact fuel tax. A sales/use tax refund is also available for producers of biodiesel. To access forms and information regarding these credits and refunds, go to our forms index.